Summary

Glycomimetics' Uproleselan is expected to read out data in relapsed/refractory and elderly newly diagnosed Acute Myeloid Leukemia (AML) after 6 years in pivotal studies.

AML is a disease with a poor prognosis, especially for elderly patients, and there is a need for better treatment options.

Uproleselan, a glycomimetic drug, aims to achieve minimal residual disease negativity and improve long-term survival outcomes in AML patients.

Written by Dan Cohen and Scott Matusow

- Introduction and primer on Glycomimetics (GLYC)

After almost 6 years in pivotal studies, Glycomimetics' Uproleselan is finally slated to read out data in both relapsed/refractory (r/r) and elderly newly diagnosed Acute Myeloid Leukemia (AML). The small-cap company has certainly taken an unusual route for its size by utilizing study designs with a rather long time to analysis. However, by doing so they may be able to establish a definitive dataset that can fundamentally change the way hematologists approach this debilitating disease.

In this write-up we will dive into key comparator studies, setting the bar for the control arm as well as the drug itself. In addition, we will examine endpoints beyond just the top-line analyses planned for these studies, and how this may inform both regulatory and commercial outcomes for Uproleselan.

- Background on AML

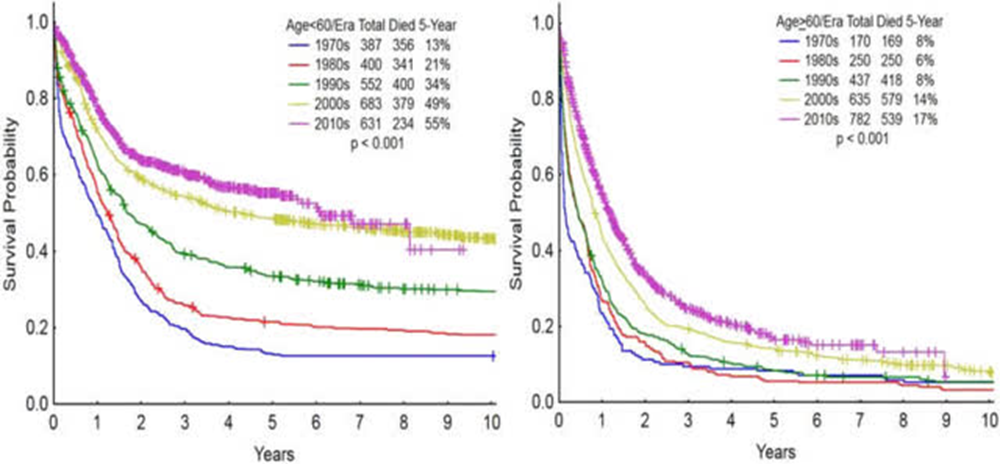

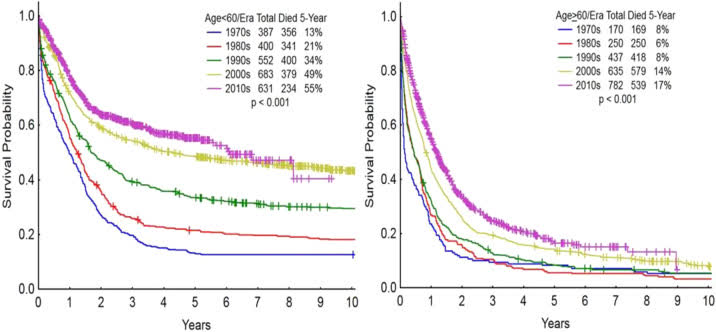

AML is a disease with significant burden on the healthcare system. According to Roche epidemiology data , approximately 22,430 patients are diagnosed every year, of whom 14,255 end up r/r. Unfortunately, there is a poor prognosis in large part because the median age at the time of diagnosis is 68. particularly for elderly patients which have a reported 9-10% 3-year survival rate. Even in the best of centers, such as MD Anderson which is shown below, there has been little progress in improving survival rates for elderly patients with AML.

GLYC Corp Deck

One of the biggest questions that hematologists/oncologists face is balancing concerns over the risk/reward of each of their treatment options. Is it worth subjecting an elderly patient to intensive chemotherapy, or should lower intensity regiments be utilized? Should a patient be given stem cell transplantation? If so, should the transplantations be autologous (derived from the patient’s self) or allogeneic (donor match)? These concerns are heightened in the elderly and/or the significantly co-morbid patient populations where secondary toxicity can lead to death.

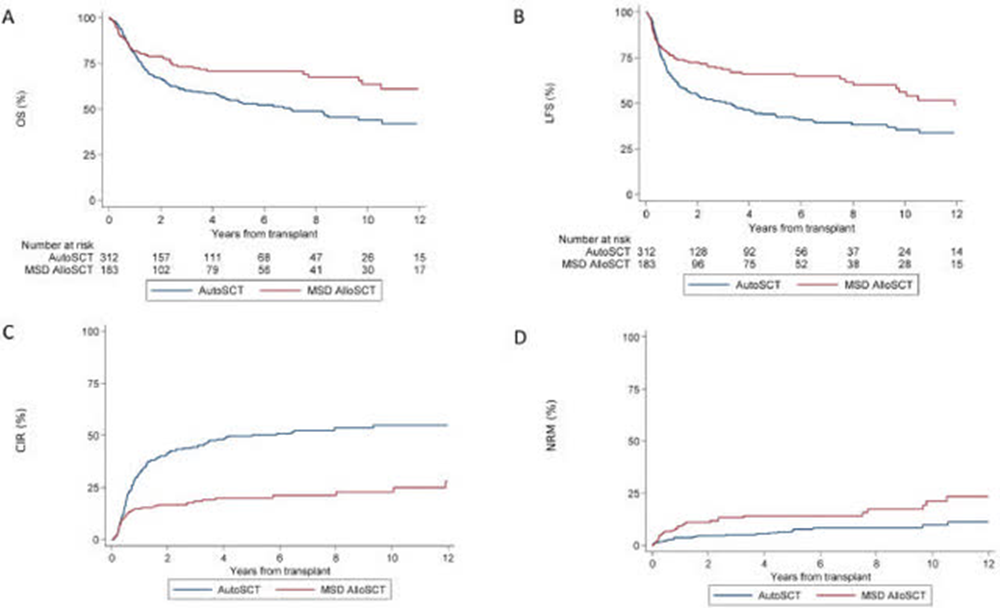

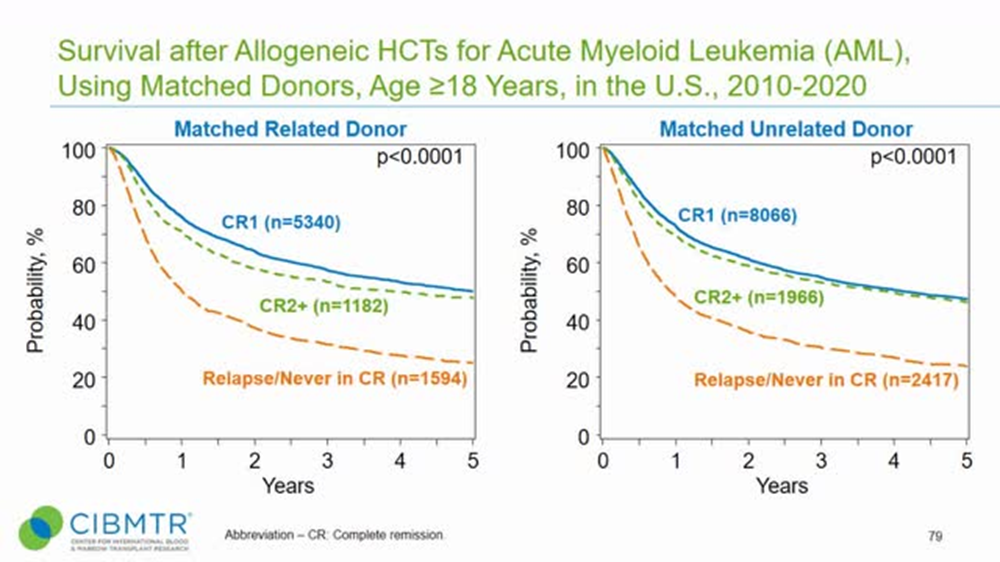

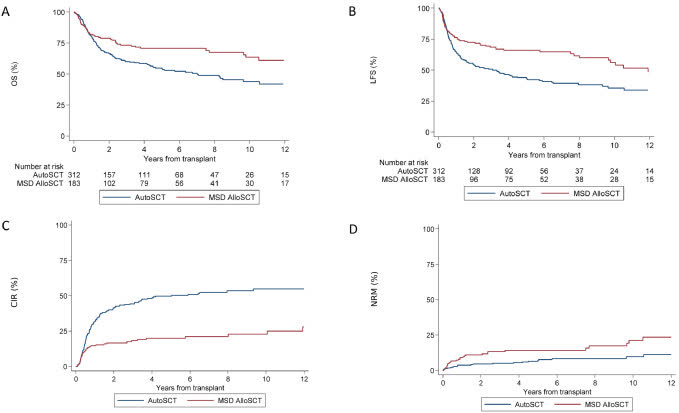

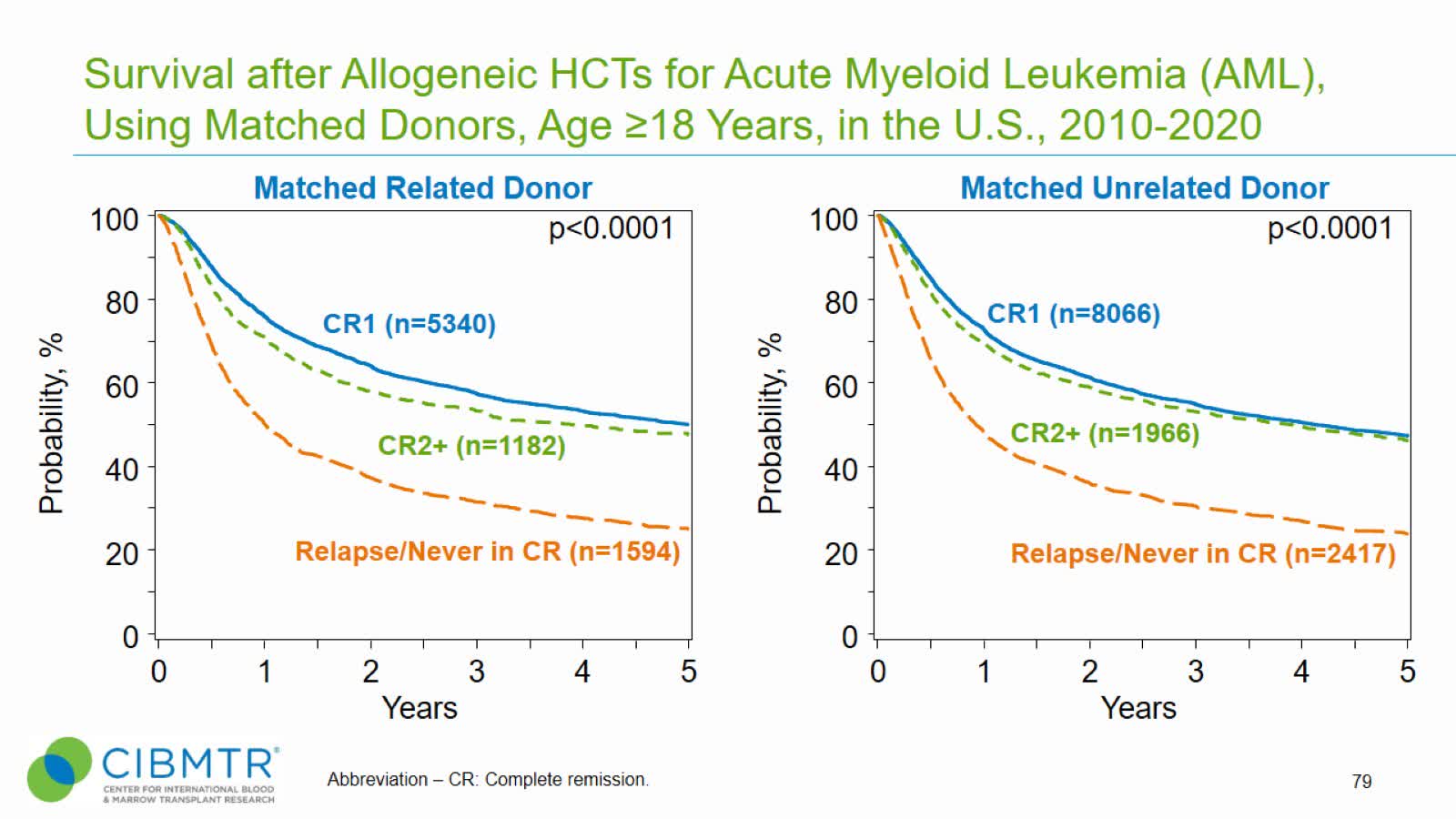

One recent publication in Blood sought to answer some of these questions in a population of elderly intermediate-risk AML patients. Notably, this is relevant to the majority of the subjects we can expect to see in the NCI/Alliance pivotal front-line AML study. In the guidance, it was found that the analysis of minimal residual disease (MRD) may be helpful in determining which form of consolidation therapy should be utilized. The authors noted that it would be preferable to offer these elderly patients autologous transplantation or lower intensity chemotherapy in consolidation should they achieve MRD negativity during induction treatment. Whereas patients who achieve a complete response but remain MRD positive should be offered allogeneic transplantation instead to potentially convert those subjects to MRD negative status. When utilizing this approach, the outcomes for MRD negative autologous match MRD positive allogeneic. This stands in contrast with conventional wisdom among physicians who typically push for allogeneic whenever possible due to the reported improvement in survival outcomes summarized below.

GLYC Corp Deck

The problem with allogeneic transplantation is that it comes with a significant host of complications, particularly for an elderly population. The most successful transplantation procedures are performed following myeloablative therapy, which is often poorly tolerated in this population. Some hematologists/oncologists attempt to reduce the intensity of the pre-transplantation conditioning, at the cost of higher relapse incidence.

In addition, the procedure is associated with complications such as acute Graft versus Host Disease (GvHD) which occurs in an estimated 30-60% of patients. In small amounts, GvHD can actually contribute to improved outcomes for patients. However, acute flares can lead to significant complications and are very difficult to manage in elderly patients. The mainstay approach is to utilize corticosteroids at the risk of potentially life-threatening infections. These are significant concerns in any patient population, but in particular for a highly co-morbid elderly AML patient, which becomes a barrier to improving long-term survival outcomes. For r/r AML, the non-relapse related mortality at two years following allogeneic transplant stands at around 23.7%, and has remained in this range for two decades now. This number increases to over 34% according to another study primarily focused on elderly patients.

- Enter GLYC’s Uproleselan

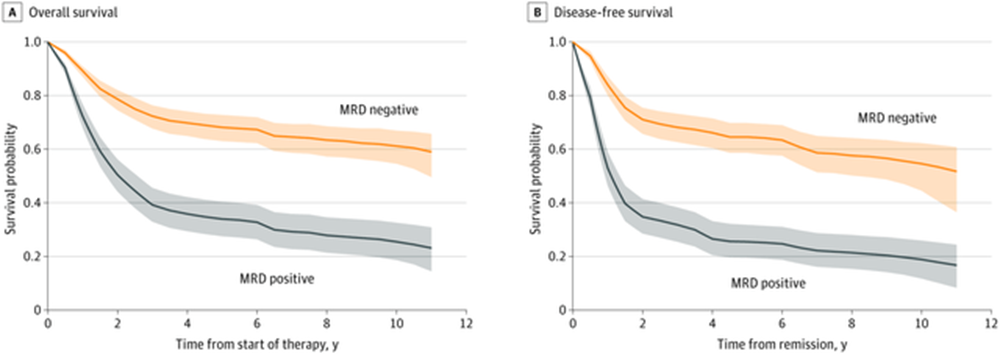

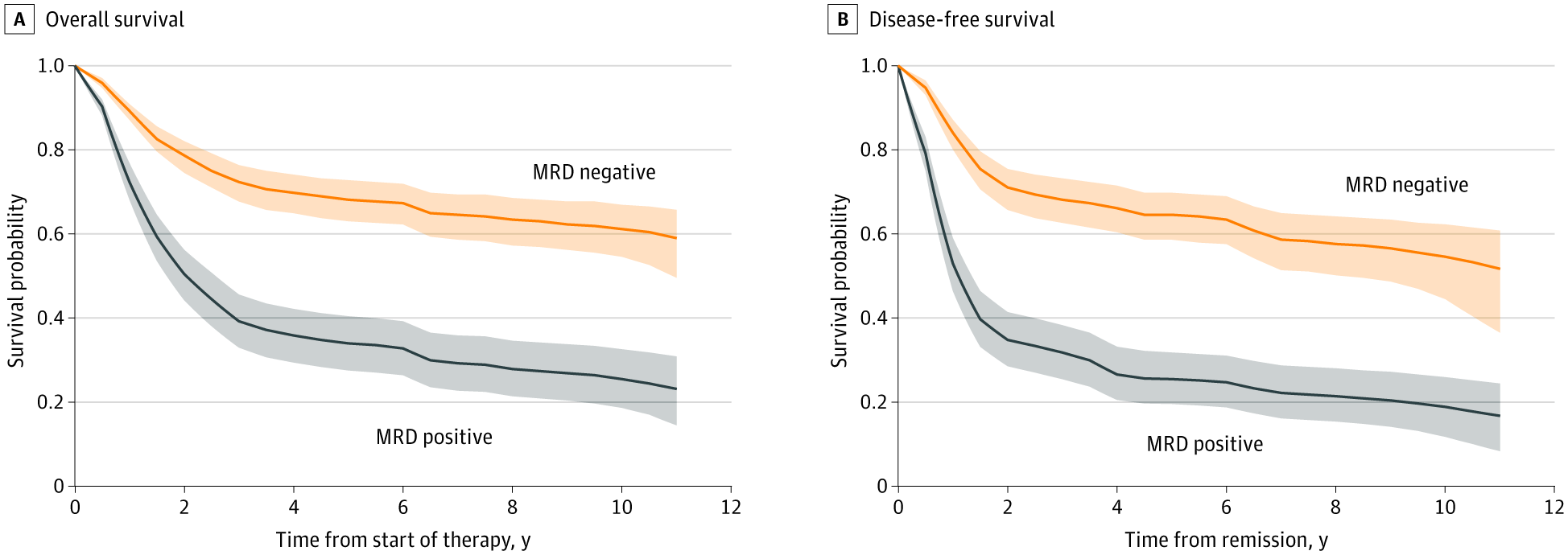

Uproleselan represents a novel class of small molecule drugs known as glycomimetics. It is designed to mimic the structure of endogenous sialyl Lewisx and competitively bind to its ligands, blocking cell-cell interactions through Endothelial (E)-selectin. E-selectin in AML is implicated in chemoresistance largely through blast binding to the bone marrow niche. Furthermore, E-selectin expression strongly associates with adverse risk cytogenetics.The hypothesis is that Uproleselan (GMI-1271) can ‘un-stick’ the tumor cells from the vascular niche and eliminate the stubborn remaining tumor cells left behind following induction therapy. In essence, achieving MRD negativity and not just a CR is the primary goal. If more patients can achieve MRD negativity, they would be able to avoid the toxicities of allogeneic transplant, which should improve quality of life and longer-term survival outcomes. The phase 1b/2 study (NCT02306291) initially posted results in 2017, sent GLYC stock from $3.82 a share to $26.05 a share (a 582% increase). The study demonstrated a significant MRD negativity rate in evaluable subjects of 69% (11/16) in r/r and 56% (5/9) in newly diagnosed. This represents a material improvement over MEC alone in r/r AML, where it is expected to achieve a MRD negativity rate of 22%. The Quiwi study (NCT04107727) which looked at a similar population of FLT3 negative newly diagnosed AML patients, showed that we can expect a 41% MRD negativity rate for the 7+3 regimen used in front-line. MRD rates in induction are highly prognostic of long term survival outcomes. Patients who achieve MRD negativity are expected to have a 5 year survival rate of 68% compared to 34% for those who fail to do so as demonstrated below:

GLYC Corp Deck

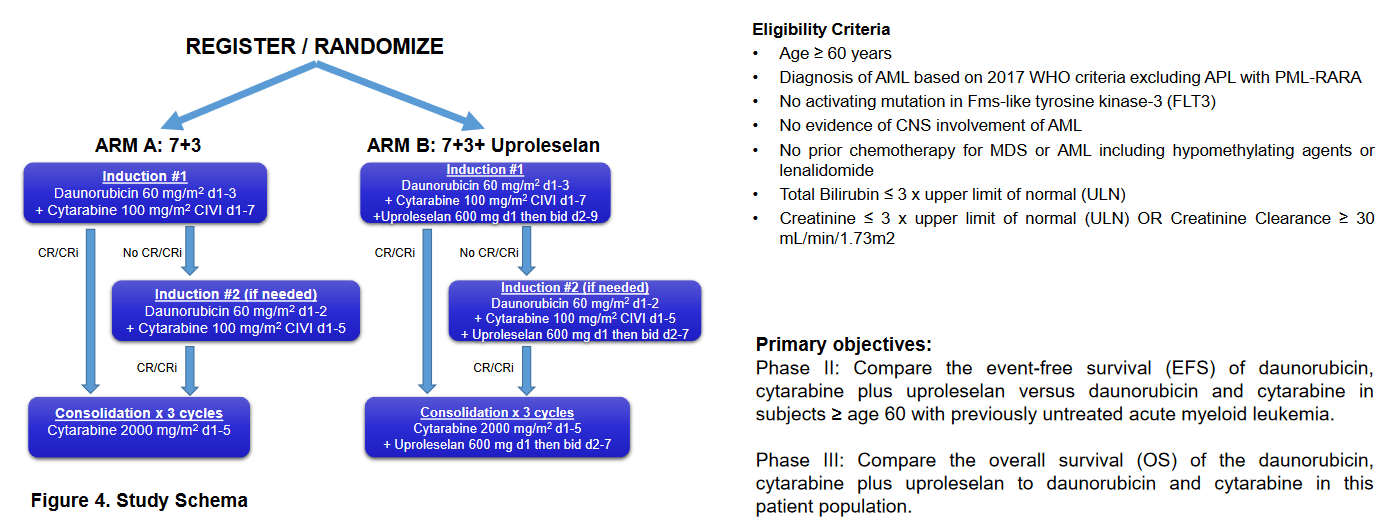

Uproleselan is being investigated in a number of settings which could help clarify not just the role the agent plays in generating MRD negativity, but also how MRD negativity plays into transplantation outcomes – these studies are listed below:

- GLYC sponsored phase 3 study in r/r AML (NCT03616470)

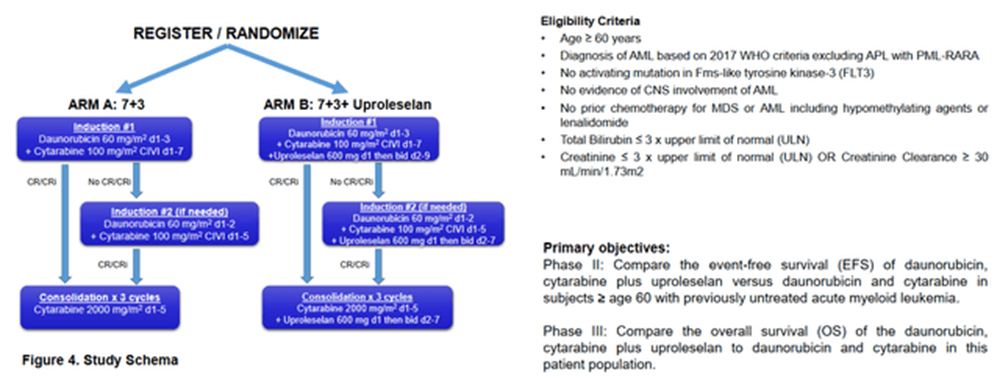

- Alliance/NCI sponsored phase 2/3 study in newly diagnosed elderly AML fit for intensive chemo (NCT03701308)

- NCI sponsored phase 1 study in pediatric patients with screened for E-selectin expression (NCT05146739)

- NCI sponsored phase 1 study run by UC Davis in newly diagnosed AML unfit for chemo (NCT04964505)

- Washington University sponsored phase 2 study in patients undergoing pre-transplant chemo for Multiple Myeloma (NCT04682405)

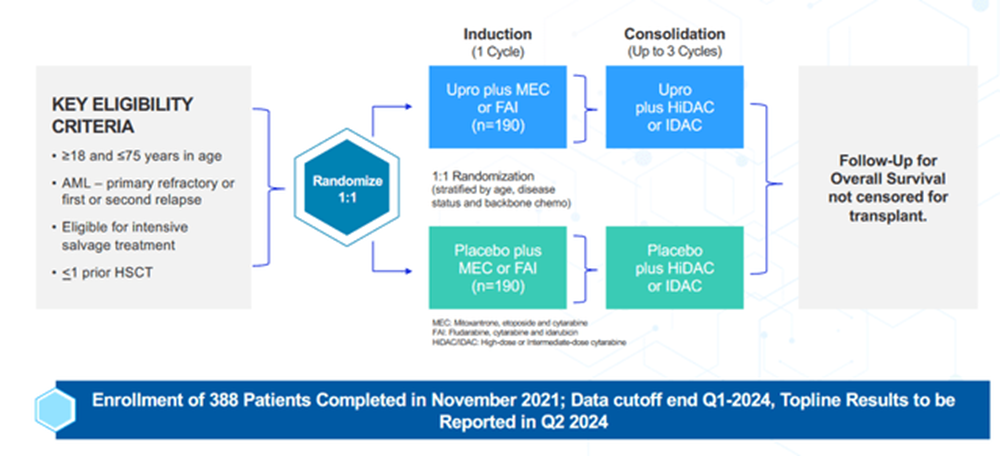

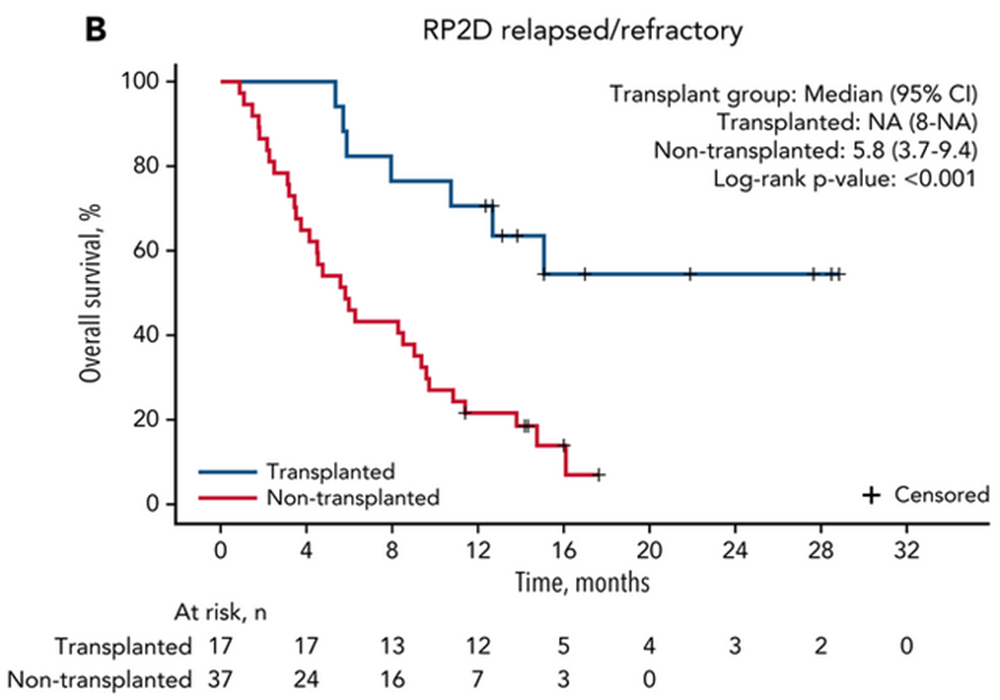

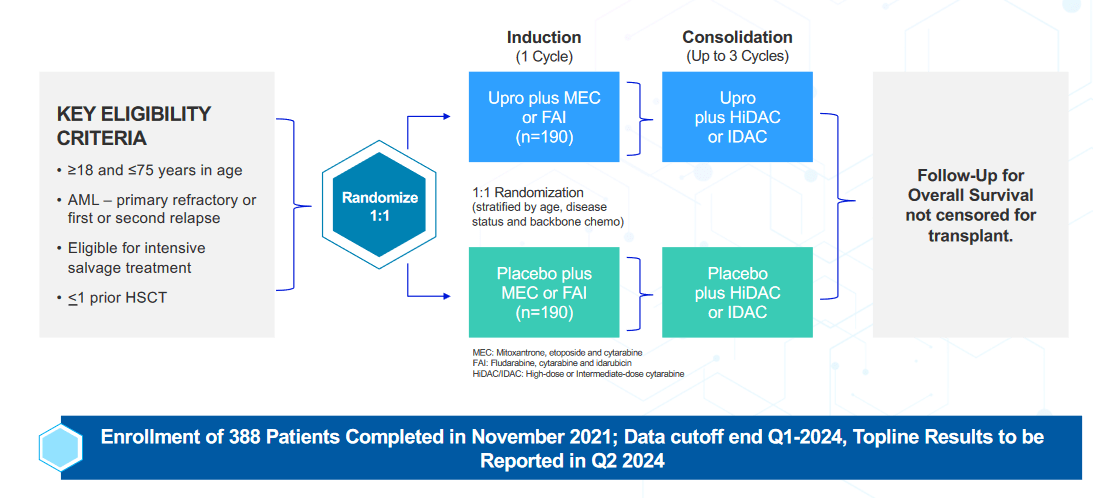

Investors should be primarily focused on the first two pivotal studies listed above as these could lead to a unified NDA filing this year (GLYC has stated they plan to use their r/r study as the anchor for registration) Firstly, the r/r study is summarized below (source: March 2024 company slides):

GLYC Corp Deck

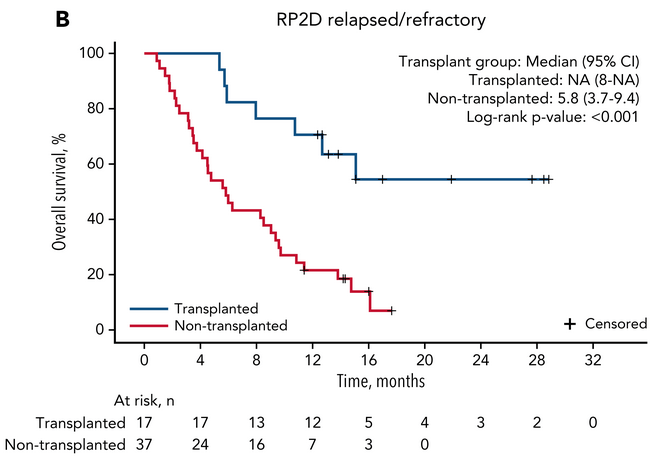

The r/r study is powered to show a 32% improvement (HR=0.68) in median overall survival (OS), in which the FDA has accepted the design as adequately powered to replace the two studies typically required for a full NDA filing. When looking at historical comparators for salvage chemo like MEC or FAI, we can reasonably expect the median overall survival to be in the range of 5.1 to 6.8 months. Meanwhile, the phase 1b/2 study (a much smaller N number which was censored for transplantation) has demonstrated a median overall survival of 8.8 months. The company has guided that the transplantation rate is “north of 31%” for this r/r study. Depending on where that lands, it may further contribute to the survival benefit. Typically, transplantation doesn’t remain durable in this setting, so clinicians can be hesitant to utilize it. However, a high MRD rate would change that outcome. Investigators on the study are being encouraged to move patients onto transplant considering both the elevated MRD negativity rate seen in the phase 1b/2 study and the meaningfully improved outcomes for those undergoing transplant shown below:

GLYC Corp Deck

Curiously, we are now sitting at 37 months of median follow-up on study, which is designed to un-blind at 295 out of 388 events. The 2-year estimated survival for a r/r AML population is estimated at under 20%, which conventional thinking should have seen this study trigger a read-out long ago. Given the extraordinarily long time to read out, the FDA in the Summer of last year accepted a time-based cut (OS-Rate) which cuts off at the end of March, 2024 (this month).Interestingly in and of itself, the same phenomenon is being observed in the Alliance led newly diagnosed study as summarized here (source: ASH 2019 Poster):

Alliance ASH Poster 2019

The front-line study is powered to show a 36% (HR=0.64) improvement in median event free survival (EFS). Should the study exceed this bar it will be returned to Glycomimetics for the company to include the data in a registrational filing (most likely as part of the registration filing for the r/r rather than an Accelerated Approval path should the frontline study prove to be successful). If the HR lands between 0.64 and 0.83, it will continue to the phase 3 portion of the study with an OS primary endpoint. If the study’s HR ends above 0.83, it will be terminated for futility. However, this trial being stopped for futility is highly unlikely in lieu of GLYC’s Ceo Harout Semerijan’s, comments in the 2021 Q4 earnings call in March of 2022, in which he stated the study had passed the “initial futility analysis.” Given that both studies recruited their last patient within less than a month of each other and have a similar median follow-up time. We consider it highly unlikely that the frontline study would be found to be futile upon the final EFS analysis. It's worthy to note that this trial has been suspended since December 6th, 2021, when the last patient was dosed. We are now close to 2.5 years since that last patient was dosed and the events needed to trigger The EFS read-out still have not yet been reached, as per Semerijan’s latest remarks at The TD Cowen 44th Annual Health Care Conference, which was held on March 4th, 2024.

In the Quiwi study, which was conducted contemporaneously with the Alliance study, Daiichi’s Vanflyta (Quizartinib) was evaluated in combination with standard 7+3 vs 7+3 alone. Similar to the Alliance study, all newly diagnosed patients (de novo and secondary AML) who were FLT3 negative were eligible. The study found a median EFS of 10.6 months for the 7+3 arm.

This establishes the upper end of what we can expect from the Alliance study, given that the population in Quiwi had a median age of 57, were exposed to 200 mg/m2 of Cytarabine, and had the opportunity to receive post-transplant maintenance chemotherapy. The Uproleselan study by comparison, enrolled an elderly population aged 60+, received half the Cytarabine dose, and did not receive on-protocol maintenance chemotherapy.Notably, Uproleselan does not add to toxicity in the same way that other anticancer agents typically do. In fact, the phase 1b/2 study showed there might be a benefit in mucositis, which an mechanistic rationale exists here that it affects endothelial cells of the GI lining.

This benefit was further interrogated in the context of high intensity myeloablative chemotherapy (high dose melphalan) utilizing in conditioning for transplantation in front-line multiple myeloma. It appears that even in this under powered n=50 study, there was benefit in reducing several toxicities which arise during conditioning and transplantation.If Uproleselan can make it easier for patients to bridge to transplant by mitigating the toxicities of chemotherapy in addition to deepening the efficacy of the chemo itself, it should be successful in both lines of the study. The transplantation rates for both the newly diagnosed and r/r studies will be key, as an elevated transplantation rate leads to better long term survival outcomes. This is supported in the CIBMTR slides

CIBMTR 2021 slides

The company believes that a MRD negative transplant is far more likely to achieve long term remission without treatment, aka a ‘cure’. This would theoretically bump up survival outcomes to have a plateau at a higher level. Notably, this study like Quiwi, does not censor for transplantation. So, any benefit from achieving pre-transplant MRD negativity will be captured in the analysis.

However, the definition and use of MRD in the context of AML is still being debated among the physician community. This is in large part due to the lack of standardization of tests versus other settings like acute lymphoblastic leukemia (ALL). Unlike ALL, AML is a polyclonal disease, meaning that patients harbor differentially mutated cells. As a result, there is also no standardization of genetic assays for the disease. So, looking for MRD which typically relies upon a genetic screen in the context of AML, is much more difficult.Both the front-line and r/r randomized studies are examining MRD, in addition to having what will be clearly long-term survival follow-ups. The poster for the Alliance study refers to a “multiparameter flow cytometry” using a ‘Different from Normal’ technique performed at end of induction and end of consolidation.”

This could be an opportunity to integrate the surface expression of e-selectin on cells into the definition of MRD in a registrational setting. Presumably, a similar approach is being taken in the r/r study, although this has not been publicly disclosed.

- Company Financials

| Balance Sheet As of Sep 23: | ||||

| Total Assets | $ 53.20M | |||

| Total Liabilities | $ 6.65M | |||

| Total Equity Gross Minority | $ 46.55M | |||

| Total Capitalization | $ 46.81M | |||

| Cash Burn Rate Per Q | Approx. $10M |

Because GLYC is a developmental biotech, the company has no income to report on. As of Q3 2023 (Q4 Yearly 10K is due on March 27th, 2024) the company has about $46M in assets/cash to get by for a few more quarters. If both their near-term data read-outs should prove to be failures, the company would be in serious financial problems and the stock price would likely be cut in half from its current range of around $3 a share, if not lower. Furthermore, the company would likely engage in a very dilutive negative raise, may reverse split, and eventually delist. In other words, these development biotechs carry huge risk, but also carry potentially massive rewards;

- Conclusion

We believe that Uproleselan has a high probability of success in both lines of AML therapy and could potentially become a backbone across the spectrum of treatment. It can function akin to dexamethasone in multiple myeloma, reducing inflammation while improving efficacy outcomes.

The unique mechanism seeks to expose cancer cells to treatment and is complementary to multiple approaches, including Venetoclax + Azacitidine, which is being explored by investigators at UC Davis. Preliminarily, half (4/8) of patients enrolled as of June 2022 have experienced a MRD negative CR as measured by multiparameter flow cytometry - this is a compelling result in a setting where patients cannot tolerate intensive chemotherapy. We find it unusual that there has not been further follow up in The UC Davis study despite cancer.gov reflecting the addition of Dan DeAngelo’s clinic at Dana Farber. He was notably the lead investigator from the phase 1b/2 study for Uproleselan back in 2017. It is unlikely that this site expansion on what should be a single center IST would take place in a study which was futile in our opinion. It is likely that Abbvie (ABBV), who has been pushing for the expanded use of Venetoclax in fit for chemo patients, would be keen to co-develop Uproleselan with Glycomimetics. We believe the backbone approach of utilizing a combination of both Venetoclax and Uproleselan should work well together in synergy. ABBV makes the most sense to us to be the optimal Co-Developer partner with GLYC. Whether or not this comes to fruition or any partner for that matter, will hinge on trial success – having the right data in-hand from which to negotiate an optimum deal for the company.

If the GLYC trials hit then the stock can rapidly appreciate like Pharmacyclics did beginning in 2009; the stock started its run at around a dollar and was ultimately acquired by AbbVie for $261.25 ($152.25 in cash and 1.6639 shares of AbbVie).

We have been calling for GLYC success since 2017 and stick by our call on this one. The company has very unique and highly differentiated chemistry that could see a whole new platform of drugs and potential cures for various diseases, and not only in AML, but also Multiple Myeloma ((MM)), acute lymphoblastic leukemia ((ALL), and potentially more.

But first things first – let’s start with seeing positive data here and then we can see a much clearer picture on the future of GLYC – we believe the company will be a big deal, so time will tell!

Disclosure: I/we have a beneficial long position in the shares of GLYC either through stock ownership, options, or other derivatives.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: This article is intended for informational and entertainment use only, and should not be construed as professional investment advice. They are our opinions only. Trading stocks is risky -- always be sure to know and understand your risk tolerance. You can incur substantial financial losses in any trade or investment. Always do your own due diligence before buying and selling any stock, and/or consult with a licensed financial adviser.

")

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}